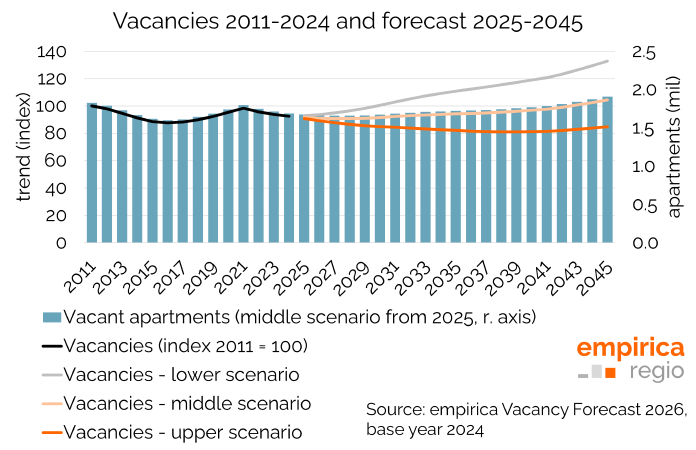

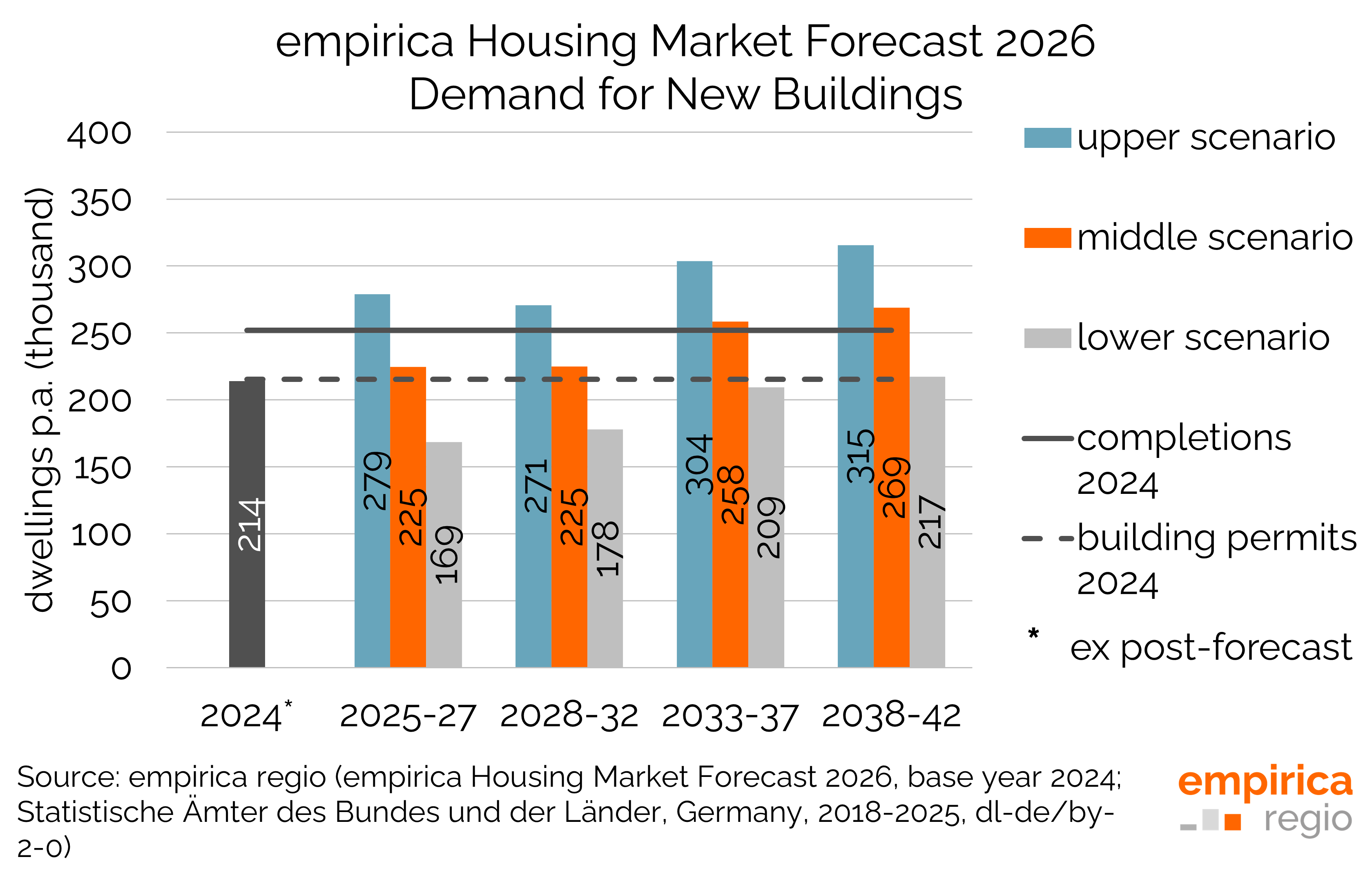

At the end of 2024, the German housing market recorded a total vacancy of around 1.7 million dwellings, corresponding to a vacancy rate of 4.0 per cent. Of the total 1.689 million vacant dwellings, 963,000 units were in apartment buildings and 727,000 in single-family and two-family houses. The situation remains particularly critical in regions experiencing population decline, where the vacancy rate could exceed the 20% threshold by the mid-2030s.