Housing bubble index Q1/2026: It all hinges on interest rates now

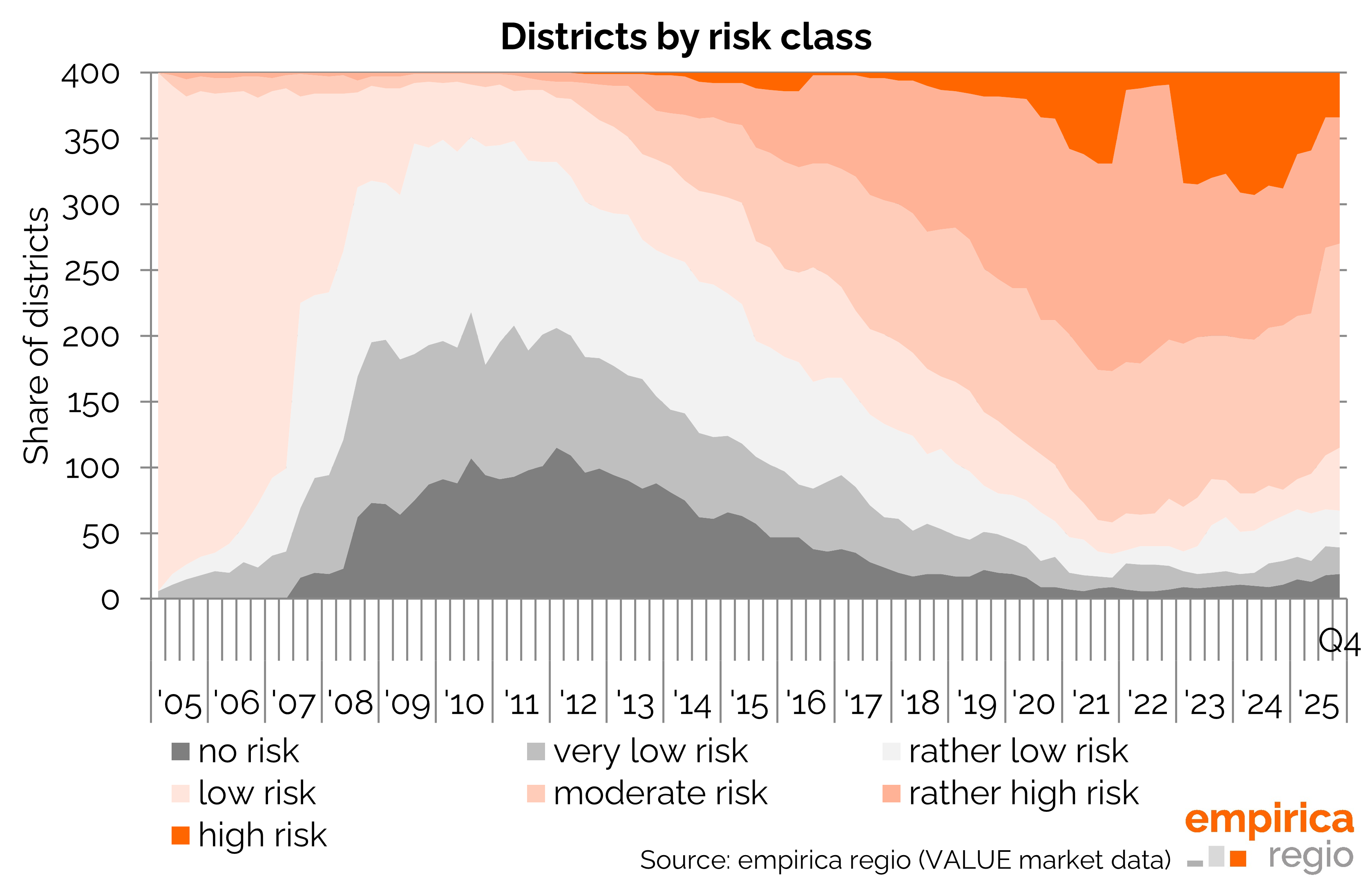

The severity of the housing market bubble risk continues to ease slightly, as rents are currently rising faster than house prices in many areas. As a result, the potential for price falls is diminishing, albeit at a slower pace than immediately following the change in interest rates. The spread of the bubble is currently stagnating, and the number of districts at risk remains high.

The current commentary: It all hinges on interest rates now – German 10-year bond yields rose above 3% in May for the first time in a long while

Developments to date: interest rates and scarcity

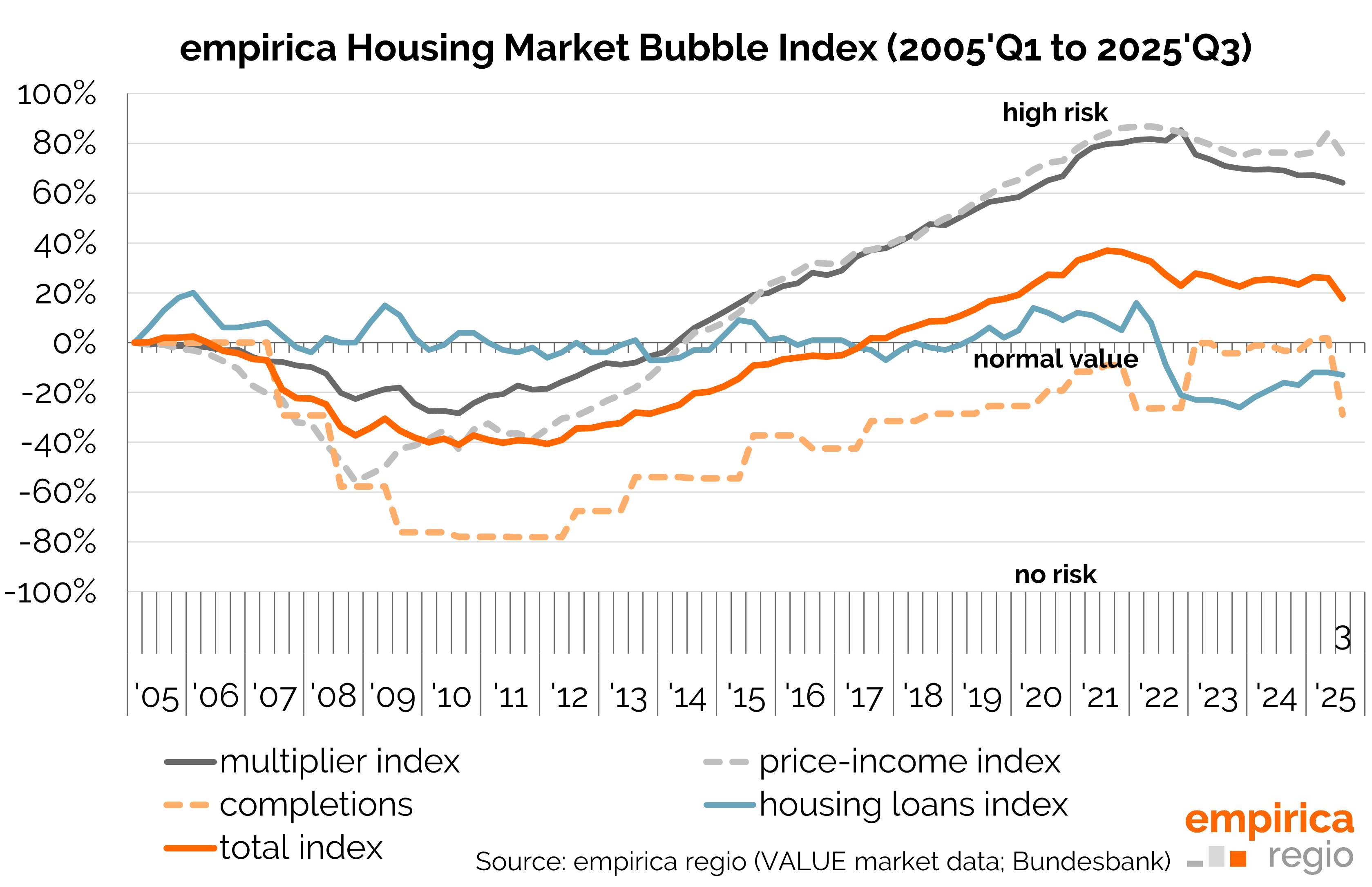

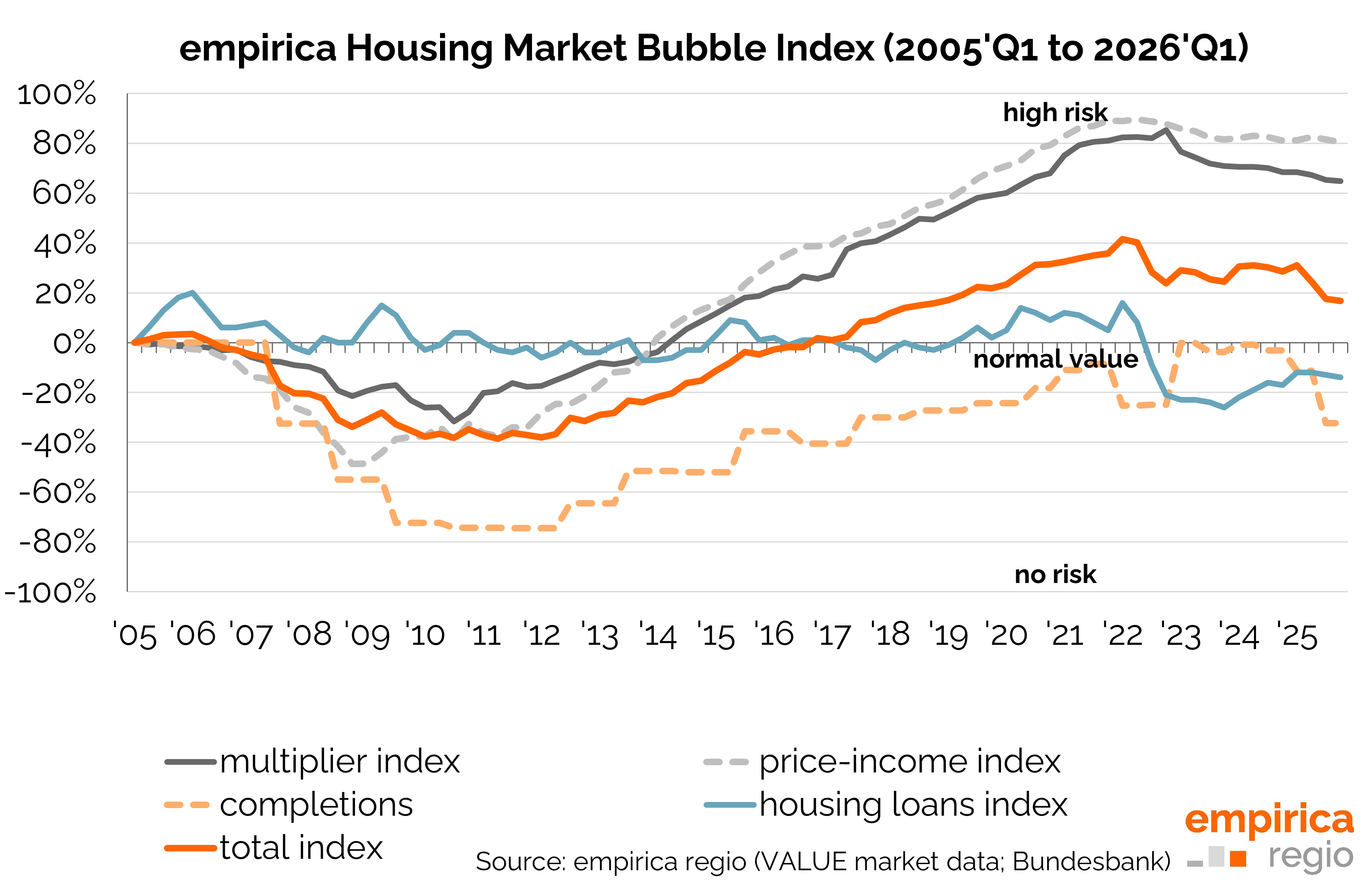

The situation remained very tense right up until 2022. Property prices – buoyed by years of low interest rates – had diverged significantly from rents (since Q3 2015: +84% for owner-occupied flats compared with just +56% for rents). A price slump seemed imminent. The rise in interest rates then brought about a turnaround: the pressure for prices to fall increased. Yet a genuine price decline has so far failed to materialise. The reason? Due to the shortage, rents are rising noticeably, thereby stabilising price levels.

Future trends: interest rates and regulation

The current trend reflects the expectation that housing will remain in short supply – primarily because new-build construction has slumped (see the ‘Completions’ sub-indicator). However, it is uncertain whether this shortage will persist. Demographic trends (immigration, structural unemployment) will be decisive in the long term. Price slumps would be more likely if the housing market eased and turnover consequently increased (e.g. through more new-builds and simultaneous deregulation of rents); for then ‘housing hoarding’ would be lower, thereby increasing the supply available on the market again and, as a result, causing new-tenancy rents to fall sustainably.

In the short term, however, other factors determine price trends: if interest rates were to rise sustainably or if rents were to be curbed by state-level clauses allowing for rent caps, this would cause the value of rented flats to plummet.

It should be noted that interest rates affect all segments equally, whilst tighter regulation could even cause rents to rise in unregulated markets – and thus mostly in the higher-value segment – but demographics have a greater impact in the lower segments: these are the less sought-after properties and less attractive locations.

Background: When do housing prices rise or fall?

When rents rise, this is bad news for those looking for a home, but good news in terms of the risk of a bubble. This is because rising rents act as a safety net for purchase prices: the value of a property is determined by the present value of future rental income. The higher the rental income, the greater the value; and the higher the interest rate, the lower the (present) value.

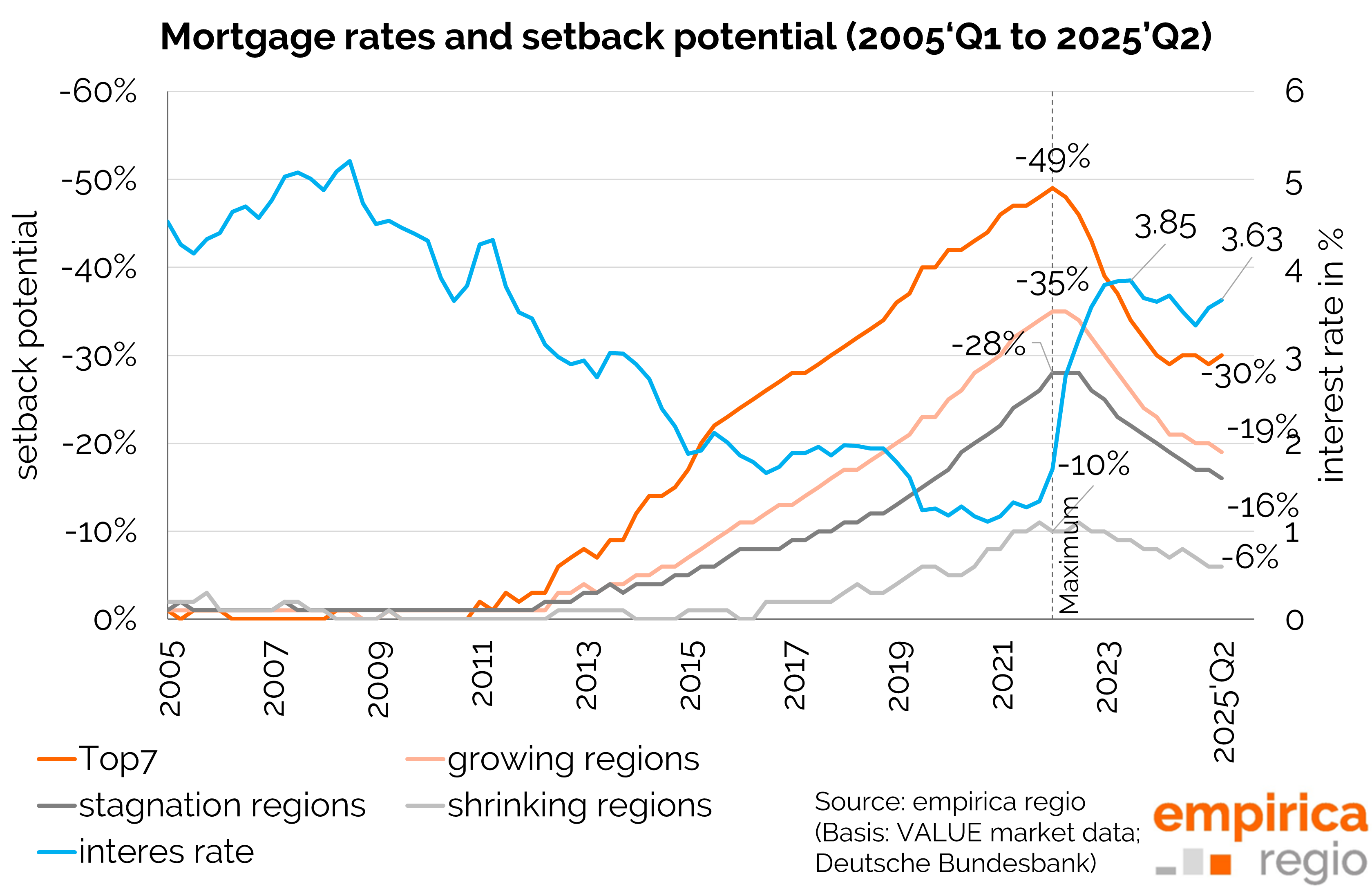

Conversely, the risk of price slumps is all the smaller the more rents rise sustainably. Rents rise not only with increasing demand or hoarding, but also when supply grows more slowly: new-build activity has fallen from 3.7 flats per thousand inhabitants in 2020 to just 2.9 flats per thousand inhabitants in 2025. No improvement is likely to be seen in 2026. Although planning permissions are currently on the rise, completions always lag behind – for multi-storey flats this can be 2–3 years; only for owner-occupied homes does it usually happen more quickly.

The relative advantages of owner-occupied housing

Incidentally, rising rents also mean that buying a home to live in is becoming a more attractive option again. This is because the higher the rent (as an alternative to mortgage repayments), the less of a burden the higher mortgage repayments for interest and capital repayment become.

Data basis empirica housing market bubble index

The empirica housing market bubble index is a quarterly index that assesses the risk of a property bubble in various regions of Germany. All data can be obtained as an individual dataset or via database access from empirica regio. Detailed results and further information on the methodology can be downloaded here: