Housing Market Data Q1/2026: Purchase Prices Show No Clear Trend

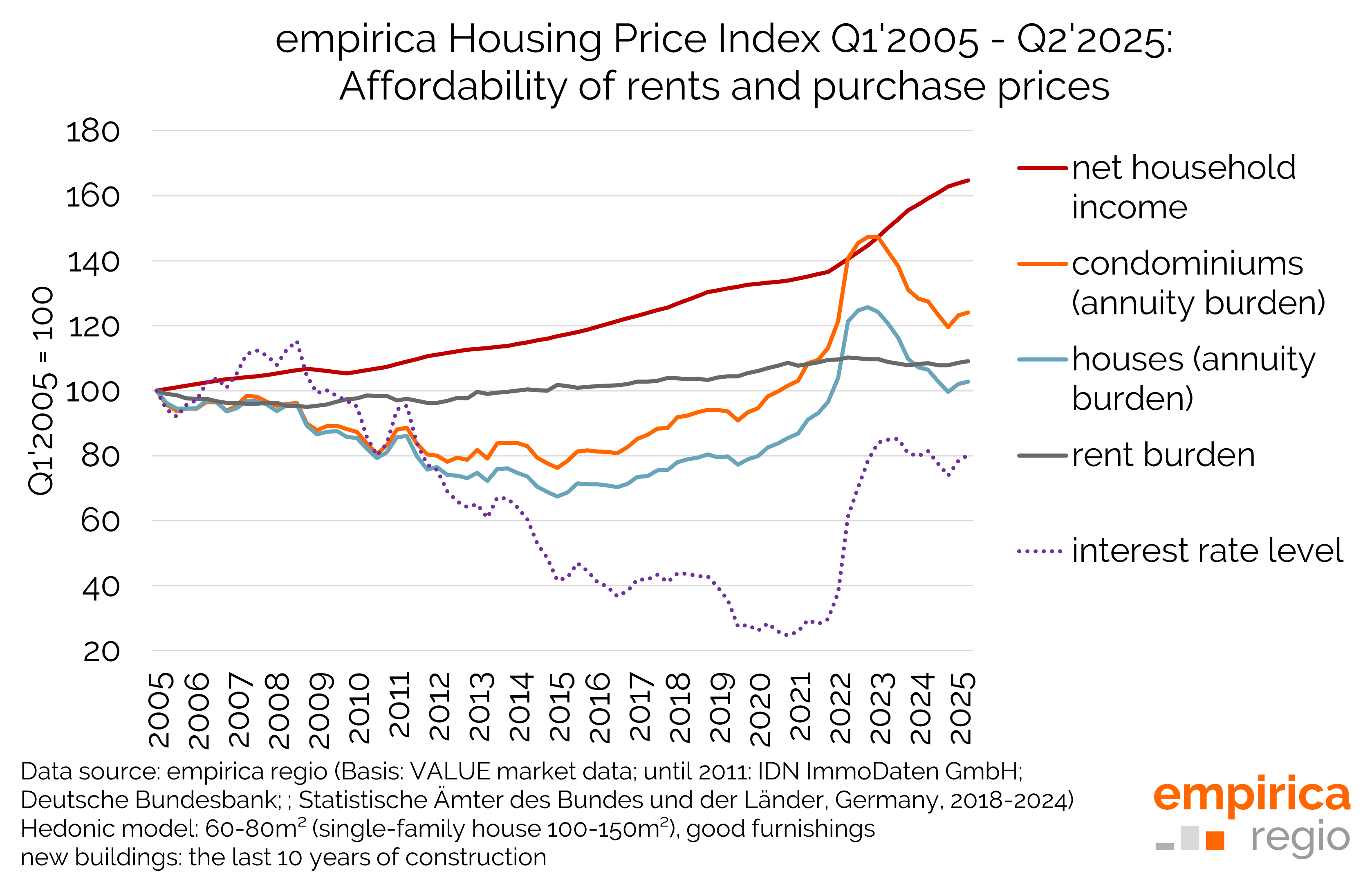

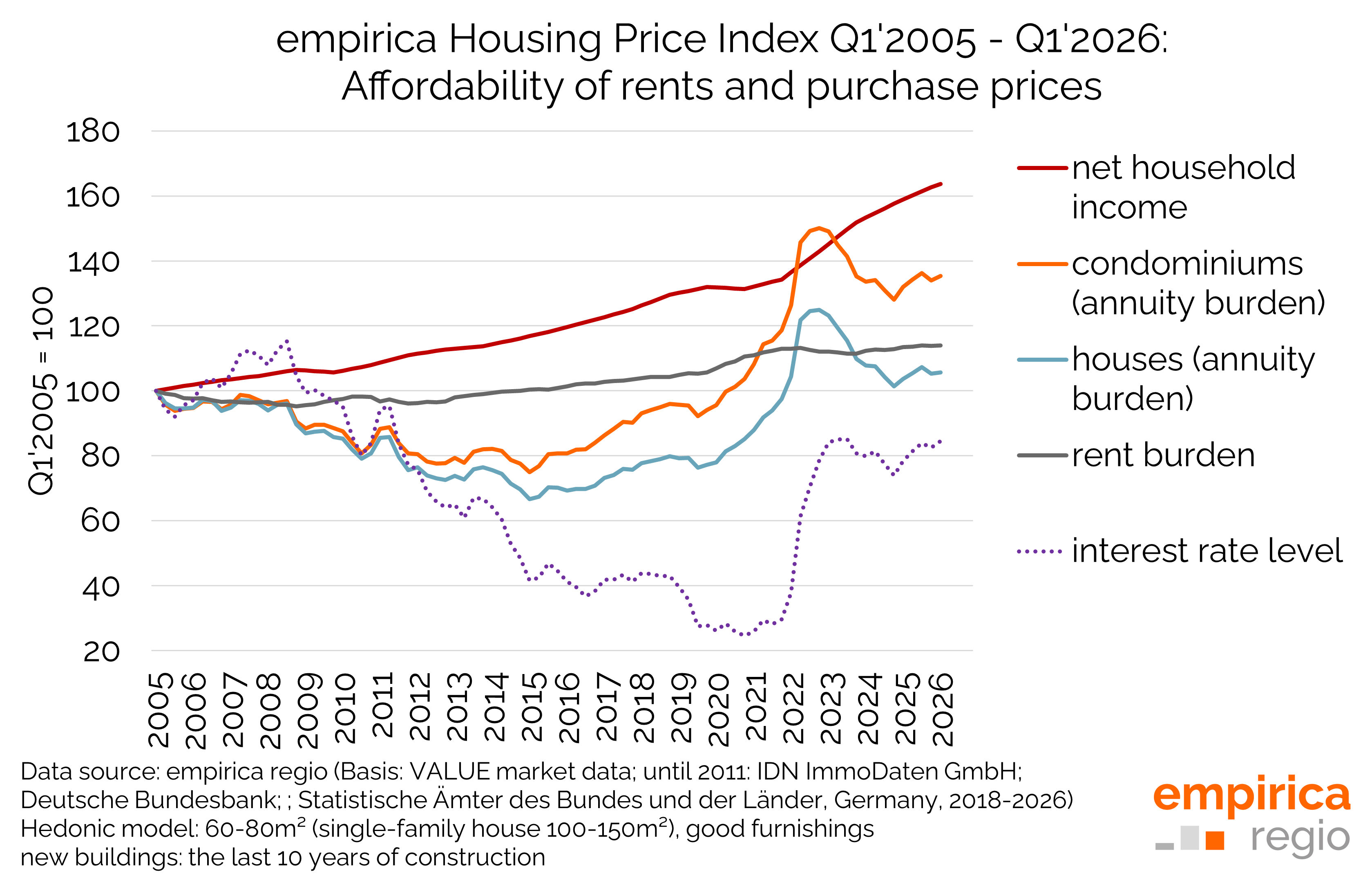

Since interest rates began to rise, advertised sale prices have recovered somewhat, as there was a severe shortage of properties and new-build construction has slumped. Affordability has also improved since then: interest rates have fallen slightly and incomes have risen significantly. However, with the current surge in inflation, the situation is likely to deteriorate again in the short term.

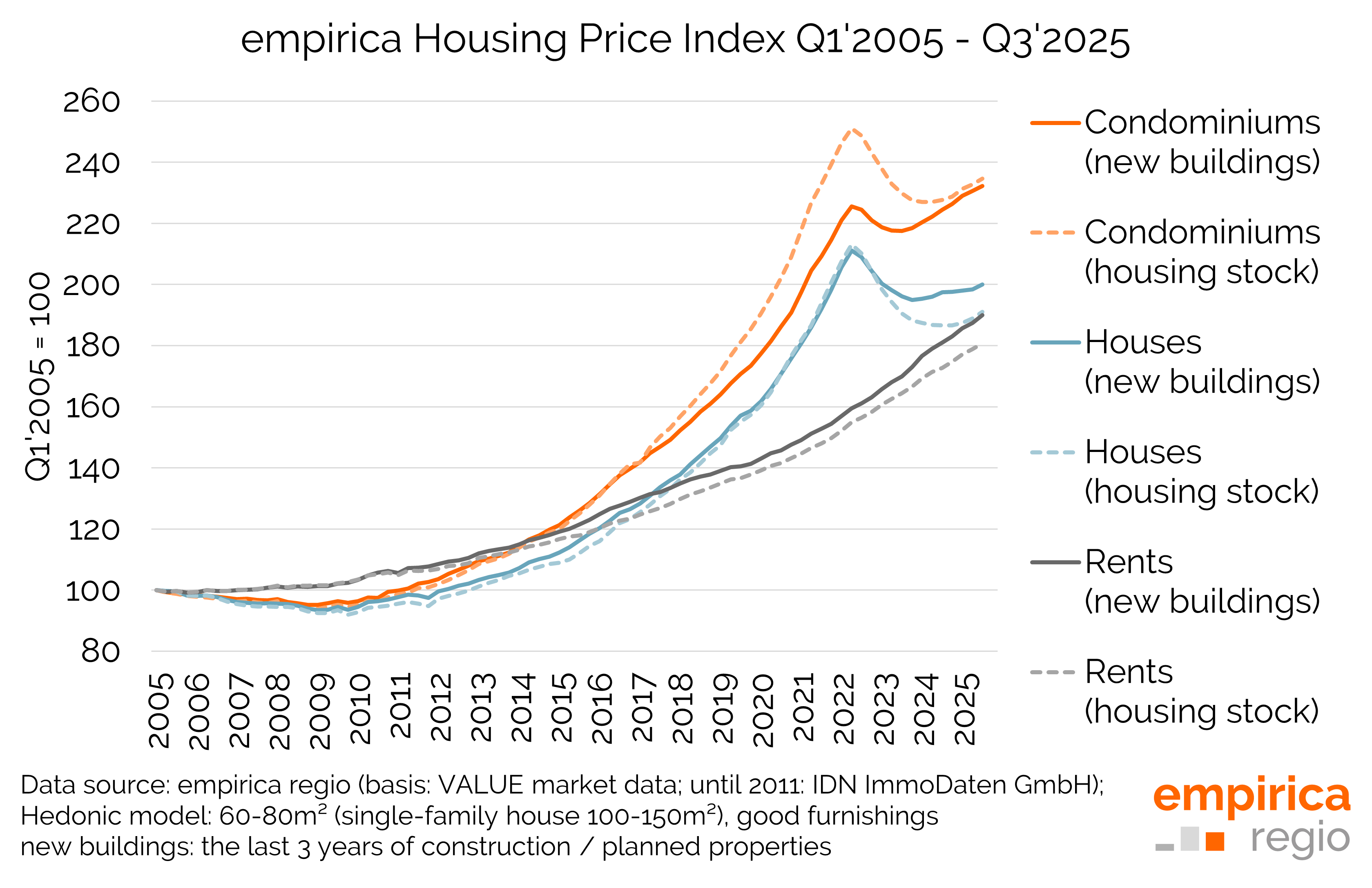

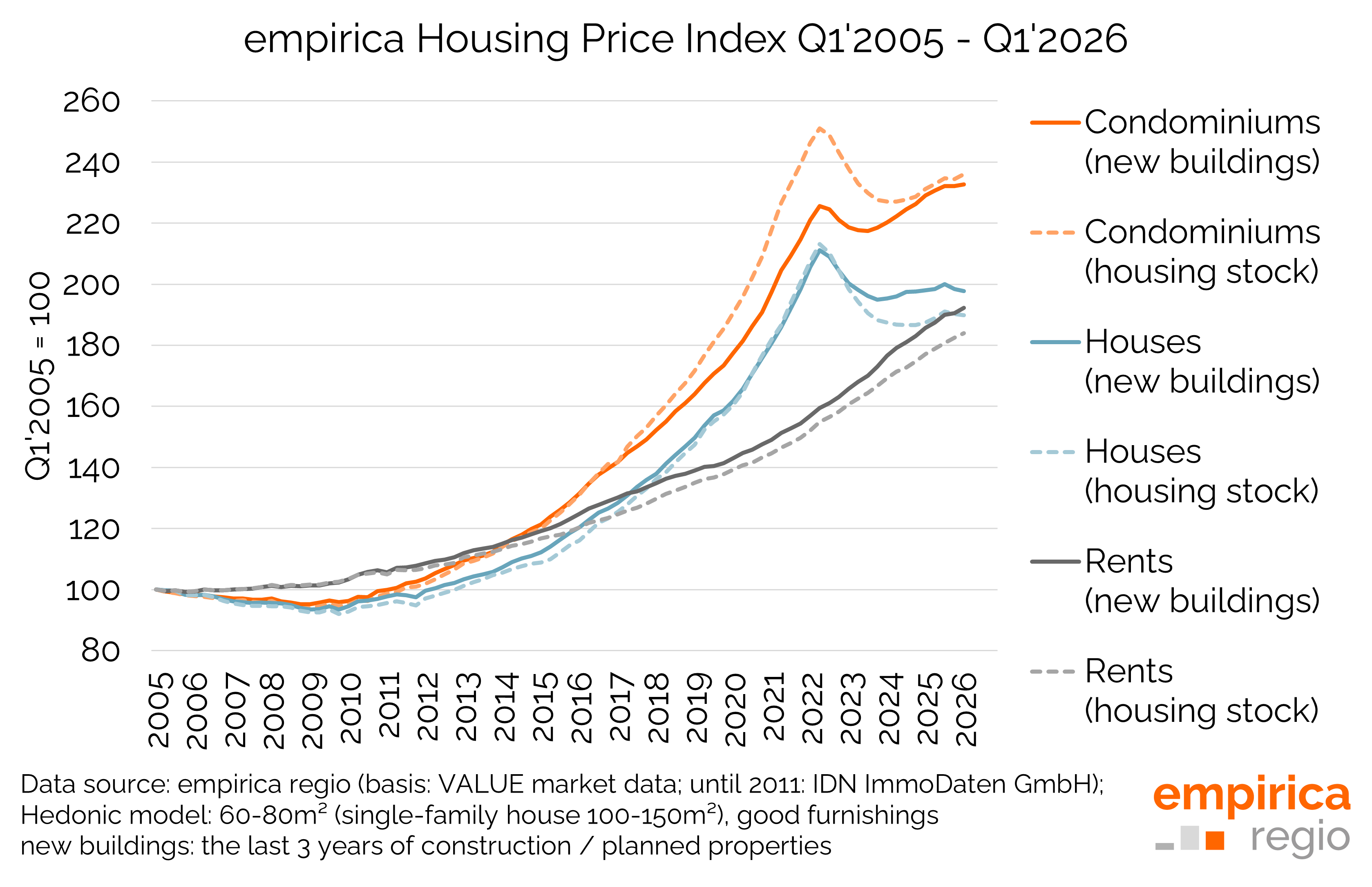

In the new-build sector, advertised prices for detached and semi-detached houses fell by 0.4% in Q1 2026 compared with the previous quarter. Compared with the same quarter of the previous year, the trend is slightly down by 0.1%. The index for new-build owner-occupied flats is slightly up by 0.2%. The year-on-year increase stands at 1.6%. For existing properties, the index for single-family homes fell slightly in Q1 2026. The decline compared to the previous quarter was 0.2%, whilst there was a 1.3% increase compared to the same quarter last year. The index for new-build flats rose by 0.7% compared to the previous quarter, with a 2.1% increase for the year as a whole compared to Q1 2025.

Meanwhile, growing uncertainty is hindering efforts to resolve the shortage. The loss of competitiveness among German companies (due to tariffs and energy prices) threatens to curb further growth in household incomes. This could take the form of slower wage growth, or even fewer overtime hours, the loss of allowances, wage cuts or unemployment.

Prices for new-build properties are tending to rise more than those for existing stock, as they are protected from falling prices by (rising) construction costs – or are not being built at all. The flood of ever-new and stricter building regulations is a major factor behind these high and rising costs. ‘Bauturbo’ or ‘Gebäudetyp-E’ are not yet really helping to bring about a turnaround in construction.

Affordability is determined not by absolute prices, but rather by the burden on income from rent or mortgage repayments. Whilst the average rental burden has remained stable in recent quarters, the annuity burden has been trending upwards again since Q1 2025 – driven by rising prices and, more recently, rising interest rates. Due to the slight price increases and the new interest rate peak in Q1 2026, the indices are now rising slightly once more.

Data basis empirica housing market index

All empirica housing market index data can be obtained as individual data sets or via database access from empirica regio. Further figures can be found in the quarterly publication on the index.